Read time: 5 minutes

Demand in the freighter sector has sparked interest from lessors; airlines; maintenance, repair, and overhaul (MRO) service providers; investors; funds; and other financial institutions. Many are keen to invest to hedge their existing passenger aircraft exposure, create new business lines around it, and/or build out their existing expertise (in the case of MROs/conversion specialists) to increase capacity and the range of conversion programs on offer. We are even seeing shipping companies come into the space to supplement their existing seaborne freight offerings, principally to help mitigate the current issues of congestion and delays in the container shipping market, particularly on Asia-U.S. routes where there are no land-based alternatives.

Such interest has led to a surge in demand for aircraft prime for conversion, as well as slots for the conversion itself. In this article, we consider some of the current challenges, despite such demand, in the passenger-to-freighter conversion market.

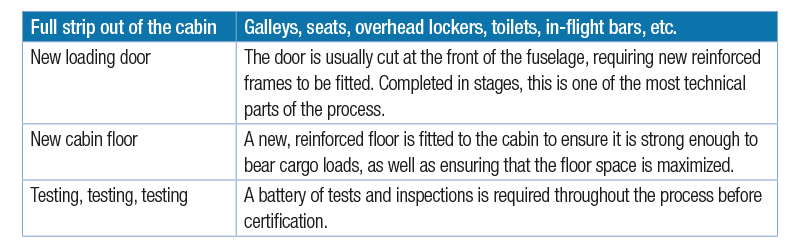

Sourcing of feedstock aircraft and conversion slots availability

Feedstock

Boeing’s World Air Cargo Forecast (the latest version of which covers the period 2020-2039, released in November 2020) states that “accelerated e-commerce adoption because of COVID-19 looks likely to extend express market growth trends.”

Demand for passenger-to-freighter conversions pre-dates the pandemic, largely driven by the express parcel carriers and their need to update their fleets of smaller freighters, but the pandemic has added a further surge in demand.

Boeing predicts the cargo market as a whole will grow at an annual rate of 4 percent over the next 20 years, resulting in the requirement for a freighter fleet 60 percent larger than we have today. Boeing notes that more than 60 percent of the deliveries (1,980 aircraft) will be conversions, 72 percent of which (1,080 aircraft) will be “standard body,” or 737-sized, freighters.

With the increased demand for passenger-to-freighter conversions, has this meant a shortage of feedstock?

There have been reports of aircraft, thought to be long retired, being brought back into service for conversion. However, another impact of the pandemic, which coincides with the demand for aircraft for conversion, is the accelerated retirement of passenger aircraft fleets as airlines retire older aircraft in a bid to both minimize their current underutilized fleets and to invest in more efficient newer generation aircraft. As such, there appears to be a demand/supply equilibrium currently in terms of aircraft available for conversion.

Slot availability issues

The bottleneck in the supply of passenger-to-freighter aircraft comes at the conversion stage, with the availability of slots at most major conversion facilities booked up until 2024, and in some instances until 2026.

Conversion facilities are being extended and new facilities set up, however, these initiatives take time:

- Boeing will expand its conversion business by setting up a passenger-to-freight facility in Costa Rica. The facility is set to come online at some point in 2022.

- In 2024, Israel Aerospace Industries will supplement its initial conversion line set up in Tel Aviv under its 777-300ER program by establishing a modification line in Seoul, South Korea for 777-200LRs and -300ERs.

- Elbe Flugzeugwerke continues to increase its capabilities. By 2024, it will increase its current capacity to the point that it will be able to produce approximately 60 converted aircraft per year – approximately 30 conversions each of the A330 and the new A321 narrow-body – up from the 19 conversions it expects to carry out this year. It also expects to establish production lines in China and the United States for the A330 reconfiguration in 2022.

Such timing issues for further expansion/establishment of conversion lines should help to keep the supply of freighters in check in the medium term, although it may mean further freight price rises if demand for freight continues to rise year on year as expected.

- Demand for freight is here to stay

- Feedstock availability does not appear to be an issue currently

- Freight pricing will remain buoyant due to the limited supply and low conversion rate of freighters