Overview of the new prudential regime

Given that Exempt CAD firms do not deal on own account, underwrite or otherwise take on principal risk, they will not be categorised as class 1 firms (so they will not be treated as if they are banks and will not be subject to the capital requirements in the current CRR/CRD regime). They will be class 2 firms (and so subject to the full application of the new regime unless they can meet all of the tests to qualify as a class 3 small and non-interconnected firm). Please see our previous alert for an overview of the classification of firms under the IFR/IFD.

Exempt CAD firms will become subject to a higher permanent minimum capital requirement (i.e. initial capital requirement) of EUR 75,000. However, this is just one element of the new own funds requirement which will require those larger Exempt CAD firms that become class 2 firms to maintain capital above the highest of three figures: (a) EUR 75,000; (b) the fixed overheads requirement; and (c) the new K-factor requirement. A class 3 firm is exempt from the K-factor requirement but will be required to meet the higher of EUR 75,000 and the fixed overheads requirement.

The fixed overheads requirement

All Exempt CAD firms will have to calculate a fixed overheads requirement for the first time. This requirement is calculated by taking one quarter of the fixed overheads of the firm from the previous accounting year. The full details of how to calculate this figure will be the subject of regulatory technical standards in due course, but it is unlikely to change much from the current approach in the CRR regime as there will be deductions for elements of variable expenditure such as discretionary bonuses and other discretionary appropriations of profit. The application of this requirement will require those Exempt CAD firms with substantial fixed expenses to hold significantly more capital (although there is time to build this up - see ‘Transitional relief’ below).

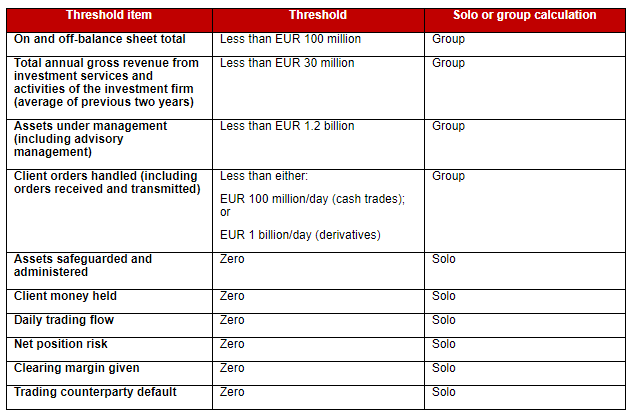

How do we qualify as a class 3 firm?

Class 3 firms are seen as lower risk and so are subject to a reduced capital and reporting burden under the new regime relative to class 2 firms. The conditions in the following table must all be met in order to qualify as a class 3 firm.

Importantly, the size tests for balance sheet size, annual gross revenue, assets under management and client orders handled are applied on a combined basis for all investment firms that are part of the same group. The other conditions are only applied on an individual entity basis. The group approach to the size tests is clearly intended to reduce the incentive for groups to restructure operations between multiple entities; however, it is likely to lead to some existing Exempt CAD firms failing to meet the class 3 tests. This will mean that they are class 2 firms and will be subject to a greater overall burden under the new regime, including the K-factor capital requirement.

Class 2 firms and the K-factor requirement

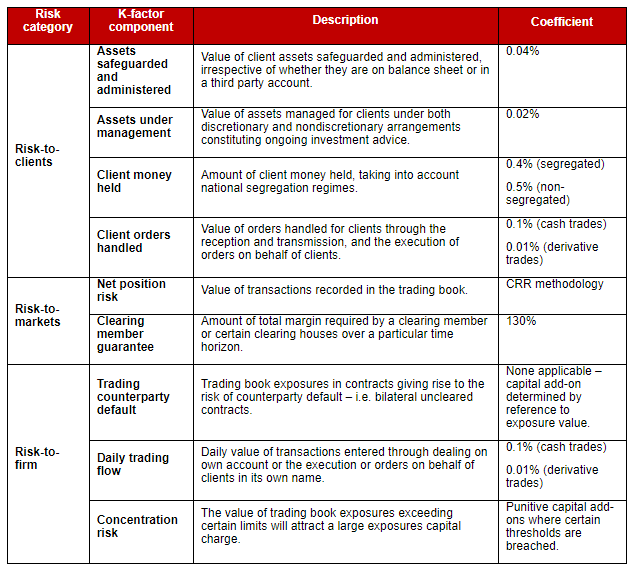

The K-factor requirement is the biggest change in the new regime. It applies percentages (‘coefficients’) to the value of specific risks encountered by firms. The new regime is intended to be a major improvement as it is calibrated to the risks of investment firms rather than banks. The risk categories and their corresponding components are set out in the following table.

Firms that are currently Exempt CAD firms will not be subject to the majority of these risk factor calculations as only assets under advisory management and client orders handled appear to be relevant. It is worth noting that assets are not counted as ‘under management’ for this purpose if a separate manager entity has enlisted the support of the adviser in conducting its portfolio management activity. The detailed scope of the K-factor calculations will be subject to additional legislation and regulatory guidance. However, there is enough in the current material for firms to begin assessing the likely impact on their capital requirements.

Class 2 firms and the ICAAP/SREP

Exempt CAD firms which do not qualify for class 3 status will also become subject to the internal capital adequacy assessment process (ICAAP) for the first time. In short, this requires firms to assess and maintain additional capital beyond that required in the normal capital requirements. This assessment is then subject to the supervisory review and evaluation process (SREP) which can lead to the imposition by the regulator of an additional own funds requirement. A class 3 firm is not normally subject to the ICAAP/SREP unless their regulator specifically requires it.

Other important changes

As well as the impact on solo own funds requirements, there are other changes introduced by the new regime.

Consolidation: some of the new rules will apply on a group-wide basis and the new regime has a clear focus on investment firm-only group consolidation (i.e. groups containing investment firms, but not any banks). This could involve regulators of firms with a non-EEA holding company requiring the interposition of a new EEA intermediate holding company. A light touch approach is available in the case of group structures “deemed to be sufficiently simple”, although it remains to be seen how this will be defined. It is worth noting that some class 3 firms may be able to apply for an exemption from the solo capital requirements and liquidity rules if they are a subsidiary in a consolidation group and the regulator agrees to such an exemption. It should be noted that if the group contains a bank, the consolidation group will be subject to CRR/CRD.

Liquidity requirements: firms will be required for the first time to maintain a liquidity cushion of cash or near-cash assets equivalent to one month of fixed overheads. Again, class 3 firms (and in some cases their parents) may be exempted from these liquidity requirements in certain limited circumstances.

Remuneration: Exempt CAD firms which become class 2 firms will be subject to the prescriptive principles on remuneration policies and variable remuneration for the first time. The new requirements are similar to the CRR/CRD regime and require firms to: establish remuneration committees; introduce limitations on certain staff around their variable remuneration, such as the payment of guaranteed bonuses, malus and clawback, the composition of variable remuneration, and deferrals; and make remuneration-specific annual disclosures and regulatory reports. Class 3 firms will remain subject to the remuneration provisions of MiFID. It should also be noted that if the group contains a bank, the consolidation group will be subject to the CRR/CRD remuneration rules. Please see our previous alert on the IFR/IFD remuneration rules.

Transitional relief

There is a five-year transitional period from 26 June 2021 which puts an upper limit on the increase in some of the regulatory capital requirements for firms; this is intended to enable the gradual build-up of capital to meet the new requirements.

Notably, firms can limit their own funds requirement to double their requirement under the current regime for a five-year period; this means that firms will have to calculate their requirements under both the old and the new regime if they wish to take advantage of this transitional relief.

The drafting of the transitional relief for Exempt CAD firms is far from ideal but the clear intention in the recitals is that firms, like Exempt CAD firms, that are currently subject only to an initial capital requirement should be able to limit their own funds requirement under the new IFR/IFD regime to twice the amount of that initial capital requirement for a period of five years from the date the new regime applies. In other words, there should be no cliff-edge for these firms, but rather they will have a maximum capital (or ‘own funds’) requirement of EUR 100,000 for five years. This will allow such firms to build their capital over that period. The Financial Conduct Authority’s (FCA’s) approach to the transitional relief should be noted (see ‘Brexit’ below) when it consults on the new regime.

Brexit

Although the IFR/IFD will apply only after the end of the Brexit transitional period on 31 December 2020 (assuming there is no extension), HM Treasury intends to take powers to enable the introduction of an updated prudential regime for investment firms in the UK. This fits with our understanding that the UK regulators were heavily involved in shaping the new EU regime. The FCA expects to consult on the detail of its implementation of the new regime in Q3 of 2020 – this has understandably been delayed by its work on COVID-19 business disruption.

Next steps

While the full detail of the new regime is yet to emerge, there is enough information in the published level 1 text to start planning and modelling for the new regime.

It is clear that any investment firm or group considering any form of reorganisation or acquisition in the months ahead should consider the impact of this new regime and plan accordingly.

Exempt CAD firms should also plan to take the following actions:

- Identify which group entities will be affected and whether consolidated supervision may be imposed.

- Determine the relevant class for each firm.

- Check whether an exemption from the solo requirements may be available for class 3 firms that are subsidiaries in groups subject to consolidated supervision.

- Consider which data points are required to classify the firm and uplift systems to monitor these thresholds.

- Calculate the new fixed overheads requirement and, if relevant, the K-factor requirement.

- Assess the extent to which the firm is required to introduce additional own funds and liquid assets.

- Identify current remuneration practices and assess how these may change.

- Review whether any corporate or group reorganisation could help mitigate the impact.

Client Alert 2020-364