1. 什么是LIBOR? 其存在有什么隐患?

数十年来,银行间同业拆借利率(“IBORs”)一直被用作银行之间互相借贷的参考利率。伦敦银行同业拆借利率(“LIBOR”)是全球经济的晴雨表,用于衡量银行在五种货币(美元、欧元、英镑、瑞郎及日元)和七个期限(隔夜、一周期、一月期、两月期、三月期、六月期及十二月期)之间的无抵押借贷成本,被国际金融机构及投资者广泛使用。LIBOR是由一组伦敦的成员银行提供报价并由此计算得出的平均利率。由于LIBOR是支撑全球超过300万亿美元金融合同价值的基准利率,其作为全球金融市场全球指数的重要性从未受到质疑。

但是,自2008年全球金融危机以来,某些报价行被发现人为操纵LIBOR报价,LIBOR丑闻由此浮出水面。这也引发了人们重新思考在无担保银行间融资市场中继续使用IBOR作为基准利率的可靠性及可持续性。

2. LIBOR将于何时终止,哪些交易会受到影响?

LIBOR丑闻爆发后,2009年4月,金融稳定委员会(Financial Stability Board,“FSB”)成立,其任务包括审查主要利率基准,并为现有参考利率提供合适的替代方案。2014年7月,FSB提出了改革主要基准利率(包括主要LIBOR利率)的建议,指出可以采用无风险参考利率(risk-free reference rates, “RFRs”)作为替代参考利率。

随后,在2017年7月,英国金融行为监管局 (UK Financial Conduct Authority,“FCA”)宣布其在2021年之后将不再强制要求报价行更新LIBOR报价,进一步加速了金融机构及其他市场参与者摆脱LIBOR的迫切性。

因此,于2021年后到期的以LIBOR为基准的未到期及新增贷款协议,与其他参照LIBOR交易的金融产品,都将受到LIBOR终止的影响。

3. 新冠疫情是否推迟了LIBOR终止的时间点?

就现阶段而言,新冠疫情并未推迟LIBOR停止更新的时间点。2020年3月25日, FCA,英格兰银行(Bank of England),英镑无风险参考利率工作组 (Working Group on Sterling Risk-Free Reference Rates,“SWG”)发表联合声明,指出尽管受到新冠疫情的影响,至2021年LIBOR报价终止的规划并未改变。与此同时,监管机构将继续监测和评估疫情对该过渡期限的影响。

2020年4月29日,FCA重申, 至2021年终止适用LIBOR的计划并未改变,但是监管机构也认识到了新冠疫情对相关工作带来的挑战,并推迟了与计划有关的部分里程碑日期。

4. 美元LIBOR的替代利率是什么?

作为美元利率过渡期间的监管机构,美联储指定的替代参考利率委员会 (Alternative Reference Rates Committee,“ARRC”)点名选择有担保隔夜融资利率(SOFR)作为美元LIBOR的替代利率。

5. 其他币种的LIBOR的替代利率是什么?

除了SOFR,下列利率也被挑选为其他币种的LIBOR的替代利率:

由于本文聚焦于美元的替代无风险利率,因此对其他币种LIBOR的过度进程将不予重点讨论。在下文中,美元LIBOR将被简称为“LIBOR”。

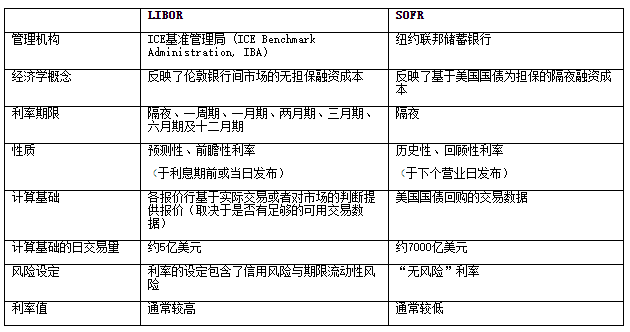

6. SOFR是什么?它和LIBOR的区别在哪里?

SOFR反映了受美国国债担保的隔夜交易成本。下表总结了SOFR和LIBOR的主要区别:

可以看到,与LIBOR相比,SOFR是根据大量实际存在的交易数据计算得出。这种计算方式的客观性使SOFR更加可靠,且更不容易受到人为操纵。

然而,SOFR仅是隔夜利率,在利息期间次日公布,并且利率值一般较低,与信贷市场参与者已经习惯的LIBOR相比差距甚大。为了使SOFR更符合贷款交易的需求,并确保传统LIBOR贷款合约的平稳过渡,需对SOFR进行以下调整:

a) 涵盖除隔夜期限外更长的利率期限结构。

b) 在利息到期日前固定利率,为借款人还款预留时间。

c) 将利率值提高至和LIBOR相近的水平。

d) 制定一套用以确定SOFR利率、计算复利以及应计利息的惯例。

6.1 前瞻性期限SOFR利率与期末SOFR复合平均值

事实上,有多种方式可实现上述 a)和b) 项的调整,鉴于相关操作细节技术性较强,因此需要单独撰文讨论。然而,最近市场上聚焦讨论的两种操作方式仍值得关注:

i.设计前瞻性的期限SOFR利率:为不同期限长短设计前瞻性的期限SOFR利率,并以屏幕利率形式公布。截至本文发表之日,这一利率尚未建立,但ARRC已定了目标在2020年9月底之前确立招标流程,以选择合适的管理机构,并在2021上半年公布ARRC建议的前瞻性期限SOFR利率(视乎市场是否能产生足够的SOFR衍生交易流动性)。

ii.计算期末SOFR复合平均值:在缺乏前瞻性期限利率的情况下,可计算“观察期”期末的SOFR复合平均值 (即运用回溯法,在利息期内的每一天都采用k天(即“滞后时间”)前的SOFR利率)。自2020年3月2日以来,纽约联邦储备银行已持续公布30天、90天和180天的SOFR复合平均值。

6.2. 息差调整

对于上述c)项所述内容,可以通过息差调整的方式,使SOFR维持与LIBOR相近的利率水平,而不同期限长短的SOFR利率可能需要对应不同的息差调整。2020年4月8日,ARRC宣布已经确立其建议的息差调整方式,并将很快发布更详细的最终建议。同时,ARRC也设立了目标在2020年9月底前确立招标流程,以选择合适的管理机构公布ARRC建议的调整息差和调整后利率。

6.3. SOFR惯例

对于上述d)项内容,ARRC的目标是在2020年7月底前就SOFR基准商业贷款确立最终建议的惯例。

7. 贷款法律文件目前处于什么状况?

7.1. 新增SOFR贷款

在欧洲、中东和非洲(EMEA)市场,贷款市场协会(LMA)于2019年9月发布了SOFR复利美元贷款协议模板草稿(后于2020年2月更新)。草稿中,任何一个利息期的利息,将参照对应观察期期末的SOFR复合平均利率计定;该观察期将于利息期开始前开始并于利息期结束前结束(即上文第6.1.ii段所述的“回溯法”)。 需要指出,该草稿仅作讨论目的,尚不构成LMA正式推荐的贷款协议模板。

与此同时,于2020年2月和3月,美国银团贷款与交易协会(LSTA)公布了两份SOFR概念贷款协议,一份基于SOFR单利,一份基于SOFR复利。SOFR复利贷款协议参照以“回溯法”计算得出的期末SOFR复合平均利率,同时含有过渡至前瞻性SOFR利率(如有)的可选条款。

7.2. 现有或新增LIBOR贷款

那么,于2021年底之后到期的LIBOR贷款该何去何从?

7.2.1. ARRC

美国市场在此方面普遍采取较开放/进取的态度。2019年5月,ARRC建议在现有或新增LIBOR贷款协议中加入“后备方案条款”,该些条款在特定触发事件发生时生效。ARRC针对三个不同的对应方法建议了三套后备方案条款:

a.“直接规定”方法(“hardwired” approach):由合同当事人预先约定替代利率和利差调整的若干后备方案以及后备方案的选择顺序。ARRC预计将于2020年6月底前更新“直接规定”方法的后备方案条款模板。

b.“议定修改”方法(“Amendment” approach):合同各方约定应于未来决定替代利率和利差调整的后备方案;该决定是否需要征得借款人的同意,则是条款模板的一个可选项。

c.“贷款利率掉期”方法(“Hedged loan” approach), 合同当事方预先约定参照国际掉期与衍生工具协会(ISDA)在衍生品交易中所采用的后备方案;此方法适用于已作利率掉期的贷款。

7.2.2 LMA

在EMEA市场,LMA则采取较为保守态度应对基准利率改革,并于2018年8月对ARRC的 “直接规定”方法的恰当性表达了顾虑,原因之一在于业界当时对于若干后备方案的细节仍缺乏充分的可预见性。

a.“屏幕利率的替换”“Replacement of Screen Rate”)条款

就目前而言,针对EMEA市场银团贷款��首选解决方案为LMA在2018年12月发布的“屏幕利率的替换”条款,该条款已纳入LMA银团贷款协议标准模板。该条款旨在降低由贷款人/多数贷款人同意变更基准利率的门槛,前提是某一贷款人没有及时提出或回复修订利率的请求。然而,就双边贷款协议而言,该条款起到的作用并不是很大。

LMA的“屏幕利率置换”条款和ARRC建议的“议定修改方法”较为相似,因在两种方法下,关于利率置换的决定均于未来作出;但主要区别在于,“屏幕利率置换”条款要求任何利率变更均需取得借款人的同意,而非一个双方可约定删除的可选项。

b. 参考利率选择协议(Reference Rate Selection Agreement)

2019年10月,LMA公布了《参考利率选择协议》草稿,允许贷款人/多数贷款人授权融资代理人根据其中条款和SOFR贷款协议建议模板(LMA尚未公布,见上文第7.1段)的要求,代表它们就贷款协议的必要修改与借款人达成一致。因此,在LMA公布其建议的SOFR贷款协议模板之前,《参考利率选择协议》并不预期会被业界使用。

c. “没有可供使用的屏幕利率”(“Unavailability of Screen Rate”)及“资金成本”(“Cost of Funds”)条款

在贷款各方无法就贷款协议的修改或者订立《参考利率选择协议》达成一致的情况下, LMA标准贷款协议的现有机制则是已被广为熟知的“没有可供使用的屏幕利率”和“资金成本”条款。简单而言,根据这两个条款,LIBOR利率按照以下顺序的备用方案决定:

- 屏幕利率(Screen Rate)→

- 推算屏幕利率(Interpolated Screen Rate)→

- [经缩短利息期的屏幕利率(Screen Rate for shortened interest period)] →

- [经缩短利息期的历史屏幕利率(Historic Screen Rate for shortened interest period)] →

- [经缩短利息期的推算历史屏幕利率(Interpolated Historic Screen Rate for shortened interest period)] →

- [参考银行利率(Reference Bank Rate)] →

- 贷款人的资金成本 (Lenders’ Cost of Funds)

值得注意的是,在实践中,合同方通常会约定排除上述第(3)到(5)项备用方案,有的时候第(6)项也会被排除。

但是,一旦LIBOR停止使用,屏幕利率(即上文第(1)项)乃至第(2)-(6)项后备方案将不复存在。作为最终后备方案,第(7)项将适用,而基准利率将不再基于或依照LIBOR,而是贷款人所告知借款人的资金成本。但是这些条款只被设计于解决LIBOR短时间内无法取得的情况,而非长远之策。此外,贷款人在判断其资金成本时被赋予较大的裁量权,这使借款人处于不利地位。最终,借款人可能会援引其请求谈判的权利与贷款人谈判,如果双方未能达成一个公平的解决方案,借款人可能需通过提前偿还全额贷款的方式退出交易。

7.2.3. APLMA

在亚太地区,亚太贷款市场协会(APLMA)通常会参照LMA的立场,并已经在标准格式的美元贷款协议中加入了旧版的LMA“屏幕利率置换”条款。根据本所的观察,这是目前绝大多数亚洲银团贷款交易会采用的条款,而双边贷款交易通常仍依赖“没有可供使用的屏幕利率”和“资金成本”条款。

8.相关市场交易

在过去的九个月里,市场上报道了一系列基于SOFR的贷款交易。

例如,在银团贷款交易方面,荷兰皇家壳牌公司(Royal Dutch Shell)于2019年12月宣布已与25家银行组成的银团就100亿美元的循环信贷安排达成协议。根据交易条款,当启用SOFR作为基础利率的市场条件成熟,SOFR将最早于合同签署日一周年后取代LIBOR利率。双边贷款方面,摩根大通(JP Morgan)于2019年10月宣布与巴西银行(Itau BBA)签订其首笔基于SOFR的双边贷款。

9.借款人应该做何准备?

本所在附录中列出了一些问题,供借款人考虑。需要指出,这不是一个详尽的问题清单,并且该些问题(或本文的任何部分)均不构成任何法律意见。

若读者有任何具体疑难或咨询,欢迎联系本所律师,他们将乐意为您提供进一步的法律咨询。

1. federalreserve.gov/speech

附录: 建议借款人考虑的问题

1. 现有的融资协议、融资函或其他金融产品合同是否采用了LIBOR作为基准利率? (例如用于计算利率、违约利率、资金中断成本等)?

2. 如果问题1的答案为是,上述合同是否有任何还款/付息日期在2021年之后?

3. 如果问题2的答案为是,该些合同是否有任何修改/后备方案条款,以及这些条款具体如何操作?

(a). 合同中是否有条款约定屏幕利率替换问题?具体采用了何对应方法?

(i).若采用“议定修改”方法(见上文第7.2.1.b及7.2.2.a段),利率更换将何时及如何生效?(是否需要所有贷款人的同意?是否需要借款人的同意?如果不需要借款人同意,贷款人/融资代理人在修改协议时有多大的裁量权?需要提前多少天通知?谁来统筹修改过程?借款人是否应联系贷款人/融资代理人提出修改请求?如果是,应于何时提出请求?)

(ii). 如果采用“直接规定”方法(参见上文第7.2.1.a段),有哪些触发事件及后备方案选项?如果LIBOR被该些后备方案取代,借款人在财务状况和操作上是否准备好?

(b). 合同各方是否签订了ISDA或其他利率掉期协议?如果是,且 “贷款利率掉期”方法 (见上文第7.2.1.c段) 未被采用,贷款协议和掉期协议中潜在的利率不匹配将带来怎样的风险?

4. 如果没有涉及利率更换的具体条文,根据合同中现有的“修订”、“没有可供使用的屏幕利率”和“资金成本”条款(见第上文第7.2.2.c段),当LIBOR停止使用时,贷款利率将如何确定?基准利率应如何修订?是否需要所有贷款人的同意?需要提前几天通知?

5. 展望将来,在没有可用的前瞻性利率而“后顾性”SOFR利率被宣布为LIBOR的建议替代利率的情况下,借款人能否在操作和财务状况层面接受“后顾性”的利率安排?借款人需要多长的滞后时间来作出付款安排?(请参见第6.1.ii段。)

6. 如果借款人是一家上市公司,当基准利率修订生效或“直接规定”条款的特定触发事件发生时,上市公司是否有任何披露或公告义务(例如给证券交易所及/或股东)?

Client Alert 2020-469